The recent pandemic created challenges for debt repayment. Many people lost their jobs, or their income levels decreased. As a result, people facing financial difficulties started looking for alternative ways of reducing or stopping their debt collection process. This is when knowing the details of forbearance vs deferment became an essential matter for millions of student loan borrowers. In this guide, we will explain fundamental differences between forbearance and deferment in the context of federal loans. Yet, if you need a long-term solution to the debt repayment problem, you will be better off with alternative solutions like Income-driven plans.

Forbearance vs Deferment

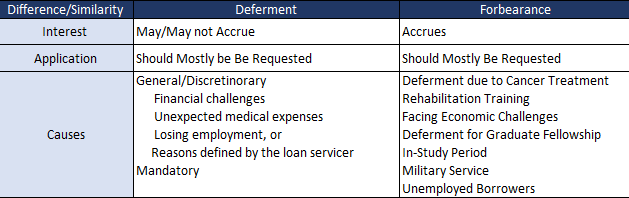

Both forbearance and deferment are alternative debt repayment options. However, they serve to stop the collection rather than repaying the debt. Borrowers who utilize one of these solutions can avoid making monthly payments for some period.

The main difference between these two debt resolution strategies is that one increases the amount of debt owed. Mainly student loan forbearance is usually less desirable because, during this period, the interest continues accumulating. Even if the borrower feels relief from debt repayment several months, they end up owing more student loans than before. On the other hand, deferment may suspend the debt collection without interest accumulation.

As student loan deferment is less costly, the borrower needs to prioritize this debt resolution strategy. However, if the deferment is not accessible and the borrower has no way of repaying the debt due to the financial challenge, forbearance can be useful.

Additionally, keep in mind that although both options can bring temporary relief, they do not help in the long run. If you think that the financial challenge will last longer, it is better to find alternatives like more affordable repayment plans. Besides, borrowers will not be able to access those options if their loans are in default. Therefore, after explaining the details of forbearance vs deferment, we will suggest some solutions if they are not accessible for you.

Deferment on Federal Loans

Deferment allows borrowers to postpone payments for some period. However, it also requires specific eligibility conditions. In general, deferment does not accrue interest payments. Yet, it depends on what federal loan you have.

Borrowers of direct, Perkins, Federal Stafford Loans, and subsidized portions of consolidation and FFEL loans qualify for deferment without interest issue. On the other hand, unsubsidized loans will still accrue interest during the deferment period. Therefore, borrowers first need to check the official website for federal student loans to confirm if they will be subject to interest accrual during the deferment.

What if I Need to Pay Interest?

If the loan accrues interest, you have two options: either paying the interest or allowing it to accumulate. If accumulated, the interest will be capitalized, which means interests will be added to the original balance owed when deferment ends. In other words, borrowers will owe more money than they got, and their total cost of debt increases.

However, here an exception also exists; if you have Perkins loans, the interest will not be capitalized. Only in the case of direct and FFEL loans, capitalization happens.

How to Request Deferment?

Borrowers in need of a deferment period should submit a request to the loan servicer. Usually, the claims are made in the written form. The borrowers can ask their loan servicers to guide and provide the necessary arrangements. In return, the servicers can ask for more documentation to prove eligibility.

How is Eligible for Deferment on Federal Loans?

Previously, we mentioned that deferment is only accessible under specific conditions. Here is a quick view on eligible causes for deferment, but we will discuss them in details in the subsequent sections:

- Postponement due to Cancer Treatment

- Rehabilitation Training

- Facing Economic Challenges

- Deferment for Graduate Fellowship

- In-Study Period

- Military Service

- Unemployed Borrowers

1. Postponement due to Cancer Treatment

If a borrower has to undergo cancer treatment, he/she will qualify for deferment. Deferment covers the period till six months after the treatment ends. Borrowers qualifying for deferment under this cause should fill the related request form and provide it to the loan servicer. Depending on the loan type owed, the deferment may or may not involve interest accumulation.

2. Rehabilitation Training

Borrowers who undergo rehabilitation due to drug use or mental disorders can get deferment with this cause. Similar to Cancer Treatment, this deferment also requires filing specific requests.

3. Facing Economic Challenges

One of the popular deferment types during the pandemic is the postponement due to economic hardship. This deferment option allows borrowers to stop payments for up to three years. The borrowers who earn less than 150% of the poverty level can qualify for this benefit. Additionally, Peace Corps servers and borrowers who receive means-tested opportunities can request deferment.

4. Graduate Fellowship Deferment

If you study in a Doctoral program, there is a high chance of qualifying for this deferment type. However, some master’s degree programs can also be eligible for this opportunity.

5. In-Study Deferment

Usually, students still studying at university are not required to make payments. In other words, they can defer the payments until they graduate and find a job. There is a six-month grace period that starts after graduation and allows debtors to avoid payments.

Unlike other deferment types, borrowers mostly do not need to fill a request form for this opportunity. It happens automatically if the borrower studies in a qualifying school at least half-time.

Additionally, parent borrowers with PLUS loans can enjoy the deferment period if their children are still enrolled minimum half-time.

6. Military Service

Borrowers serving in the military or those in the post-active duty period can request this deferment for their loans. The deferment ends when the borrower resumes studying, or 13 months pass after duty completes.

7. Unemployed Borrowers

Many borrowers faced financial challenges when they lost their jobs due to the negative impact of the pandemic. Luckily, borrowers with unemployment benefits and who look for full-time opportunities can request a postponement to stop payments for up to three years.

Important Notice for Deferment vs Forbearance

Even if you qualify for deferment/forbearance and request it, you should not stop payments immediately. Wait for the result of the request, and once it is approved, you can avoid payments. Otherwise, not making payments can put the loan into delinquency status.

Federal Loan Forbearance

As mentioned before, the main point of forbearance vs deferment is that forbearance is mostly costly- it accrues interest when the borrower does not repay the debt.

Like deferment with interest, in forbearance, the accrued interest will accrue and get capitalized at the end of the period. Additionally, capitalization is still not possible for Perkins Loans.

Requesting a Forbearance

Forbearance is not an automatic benefit. Borrowers must request this opportunity by submitting documentation and request forms to the loan servicer.

Types of a Forbearance

Previously, we explained the deferment types. The categorization was mostly based on the cause, such as having economic hardship or undergoing cancer treatment. For forbearance, the categorization is more straightforward. There are only two types of forbearance, but they also have subcategories that will be discussed subsequently:

- General/Discretionary

- Mandatory

General Forbearance

If borrowers want to get general forbearance, they need to get approval from the servicer by submitting a request. Therefore, such forbearance is up to the loan servicer’s discretion. A borrower with Direct, FFEL, and Perkins loans can apply for postponing repayment through this option. The forbearance can only be requested if the borrower has a qualifying cause such as:

- Financial challenges

- Unexpected medical expenses

- Losing employment, or

- Reasons defined by the loan servicer

As a result of proving the case for forbearance, the borrowers will be able to stop debt-collection for around a year. Each debtor can request the forbearance up to three times, creating a total three-year limit for this opportunity.

Mandatory Forbearance

As its name suggests, you will get it without question if you qualify for a mandatory forbearance. In other words, the loan servicer cannot influence this decision. However, such forbearance has strict eligibility requirements. You might be able to request the mandatory forbearance if you:

- Serve in AmeriCorps/National Guard Duty

- Participate in Defense Department’s SLRP

- Serve in Medical/Dental Internship/Residency

- Teach as Mandatory Service for Teacher Loan Forgiveness

- Have monthly payment of 20% more than the monthly gross income

The Downside of Forbearance/Deferment

When borrowers stop repaying the debt, interest can accrue. This problem is more visible in the forbearance option because deferment mostly avoids it. However, if the deferment for unsubsidized loans, interest can still be accrued.

Accumulated interest is usually capitalized- added to the original loan balance. Hence, later interests charged on increased principal balance will be even higher. In other words, interest capitalization will raise the monthly payment amounts.

Another drawback of postponing payments is related to federal aid programs. Borrowers can apply to forgiveness programs to eliminate the debt. Some forgiveness programs require repayment for a specific period to qualify for the debt cancellation. If the borrower requests forbearance or deferment, the postponed payments will not count toward the progress for forgiveness opportunities.

Consider Income-Driven Repayment

Because of the downsides of forbearance and deferment, experts usually advise finding alternative ways during financial challenges. If your income is reduced, it might be a better idea to move to Income-based repayment plans rather than postponing the payments.

Income-driven plans take the revenue as a base; hence, if your income is low, the monthly payments will be low as well. Therefore, such repayment options are more affordable for borrowers with financial struggles.

What if My Loan Defaults?

Unfortunately, borrowers with defaulted loans cannot apply for deferment or forbearance. However, it is possible to request these benefits if the loan is still in the delinquency period. Therefore, borrowers need to avoid defaulting on their loans or find ways to deal with them.

Sure, the best way is to repay the debt if the loan defaults. Understandably, not every borrower can afford such a debt resolution strategy. In such cases, borrowers can utilize either student loan consolidation or rehabilitation.

Loan consolidation involves paying off a defaulted loan with a new consolidation loan. Borrowers need to make three consecutive payments before applying to this solution. Meanwhile, loan rehabilitation involves making nine payments consecutively to eliminate student loan default status. After the default status is raised, you can apply for forbearance or deferment.

Final Words

Forbearance and deferment allow borrowers to postpone their debt payments for some time. There is no significant difference between the applicable time, which is usually up to three years. However, the main dissimilarity is that forbearance is almost always more costly. During the forbearance, interest payments accrue. Such downside also exists for deferment, but it is possible to get deferment options where interest does not accumulate.

Besides, the causes on which the debt forbearance vs deferment is requested can vary. Borrowers need to fill a request form for deferment while it is possible to get automatic forbearance under the mandatory postponement type.