We all need urgent money from time to time. Whether it is for medical, personal, or educational matters, we might need to get access to cash in a short time. Luckily, there are lenders like Elastic who make requesting cash advances fast. Elastic gives access to the credit line whenever a borrower needs it. There exist some eligibility requirements and credit limits; yet, it can approve an application in as short as one business day. Sure, getting money fast is an attractive option, especially if you need to finance education or pay the existing loans. Hence, Elastic can be seen as an alternative to student debt. However, borrowers should not get too excited about Elastic student loans and evaluate the opportunity thoroughly before applying for it.

This guide will discuss the cash advances through Elastic in detail, including the repayment options, costs, eligibility conditions, application process, etc. Besides, we will present the alternatives to Elastic student loans so that the borrower can choose the most cost-efficient way to finance their education.

What is the Elastic Line of Credit?

If you need immediate access to funds, the Elastic credit line provides an easy way. The loan provider aims to ensure that the customer gets the money whenever he/she needs it. Elastic achieves this goal through its fast and straightforward application process. All it takes is opening an account and activating it to get access to money.

When a borrower requests money, the company deducts a fee from the request and then delivers it by check or to the checking account. When the customer repays the amount, he/she can request more cash advances within the credit line limit.

The credit limit is usually between $500-$4,500.

Payments to Elastic

Not only getting the money but also repaying it is simple. If you want to finance education with Elastic, it can be seen as getting Elastic student loans requiring payments. Like the loan repayment, the individual needs to make minimum payment until the due date. The minimum due amount can include the requested amount, fees, and past-due obligations.

However, different from other student loans, Elastic student loans give the customers flexibility. The customer can choose a billing cycle and due dates based on the pay date. It is possible to customize the repayment process through the Elastic application.

For example, if you get a salary weekly, you can decide to repay these funds for education weekly. Alternatively, options like bi-weekly, semi-monthly, or monthly exist.

If a customer wants to move from one frequency plan to another, he/she needs to contact the customer service. However, keep in mind that the transfer to different frequencies can change fees and minimum payment amounts.

Repayment Options

Besides frequency determination, Elastic student loans’ repayment provides different methods to complete the payment.

If you searched for private student loans, you probably noticed a useful feature in such loans, Auto-pay. This feature is also available in the Elastic line of credit, and it allows the company to automatically deduct the payments from checking accounts. In this way, the borrowers do not need to worry about missing due dates.

Another method to pay the required amount is through phone, using a debit card. If your bank allows you to add different bill payments, then you can also add payments to Elastic in that list. Alternatively, using mail to send a check or money order to meet the debt obligation is also possible. Lastly, borrowers can schedule a one-time electronic payment online.

Besides, keep in mind that it is possible to pay the full amount requested or make partial payments.

Billing/Statement

Once you get the cash, the first payment due is a minimum of 14 days after the cash advance date. It depends on the frequency that the borrower prefers.

At least 14 days before the due date, the borrower will receive the statement. The statement shows many details, including balance. It is possible to access the statement online on the official platform. Besides, Elastic will inform you about the statement generated by email. In some cases, if required by the law, the statement is also sent to the mail address.

Cooling-Off Period

When student loan borrowers have easy access to funds, they might lose track and rely too much on the debt. Therefore, the borrower never ends debt payments and even accumulates more.

Elastic recognizes this problem and wants to contribute to the responsible lending/borrowing process. Hence, if a customer has a balance on an Elastic account for consecutive ten months, the company stops providing more cash advances.

In other words, the cooling-off period allows borrowers to satisfy existing obligations and to fully repay the balance without making new requests for cash advances. Sure, after the existing balance is entirely closed and kept empty for 20 days, the borrower can continue getting cash advances. Please, keep in mind that it can take up to 5 business days to reinstate the cash advance request function.

Cash Advances with Elastic vs. through Credit Cards

We call the Elastic cash advance offer Elastic student loans in this guide because our main target is students who need to finance their education. However, understandably, the offer of Elastic- cash advance through credit line- can seem similar to getting cash from a credit card, whenever needed. However, there are significant similarities and differences, which we will discuss in the following section.

Similarities

Both Elastic student loans and credit card cash advance have a certain limit. Before, we mentioned that the Elastic credit line allows getting $500-$4,500. Besides, both cash advance techniques are revolving. It means, once the borrower pays the balance, he/she can use the paid portion again.

However, keep in mind that after ten consecutive months of open balance, Elastic will stop cash advance requests. Lastly, both Elastic and credit card providers can require fees when the borrowers request money.

Differences

There are differences between Elastic personal credit line and credit card cash advances despite many similarities.

Although both methods have credit limits, the credit line’s limit is usually higher than what credit card providers offer. Next, credit cards can require lower monthly payments. However, keep in mind that with minimum loan payments, it can take years to finally pay off the debt. Lastly, when customers request money from credit cards, they can face additional charges based on their bank policies or ATM machine.

Costs of Elastic Student Loans

Before creating an account in Elastic to request cash advances, you need to evaluate all your student loan debt options. We will discuss the alternative options in the following section. This section will present the costs of Elastic student loans, or in other words, credit lines.

Elastic cash advances require two types of payments- cash advance fee and carried balance fee. The fees depend on the number of billing cycles and the type, such as bi-weekly or monthly.

Luckily, there are no other fees like application, late payment, or annual fees besides the two mentioned types.

Cash Advance Fee

First, you need to know that you will be required to pay a cash advance fee every time you request cash, which is around 5-10% of the requested amount. The company will deduct this fee before providing the rest of the cash to the borrower.

The rate is 5%if the payment is bi-weekly or semi-monthly. For example, if you request $500, the company will deduct 5% (which is $25), and you will receive only $475.

On the other hand, the cash advance fee is 10% for the monthly billing cycle. Again, for $500 requested, the company deducts 10% (which is $50), and the borrower only gets $450 at hand.

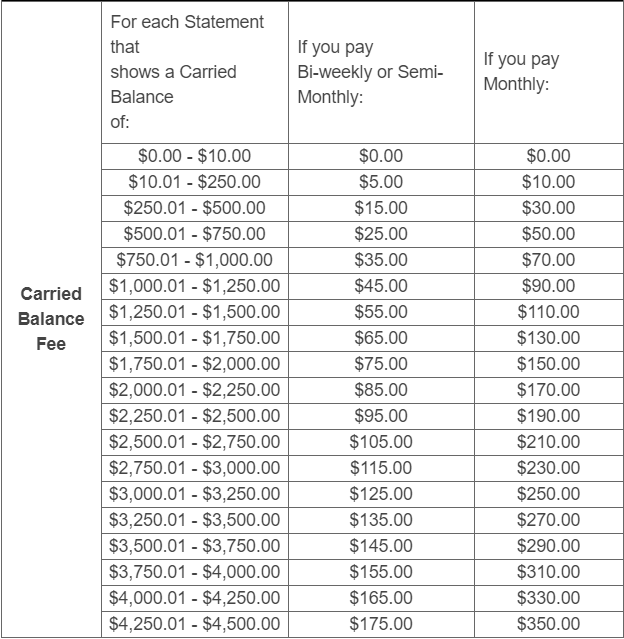

Carried Balance Fee

Understandably, individuals might not be able to repay the balance in one billing cycle. If they need more cycles, they will be required to pay an additional -carried balance fee- for each billing cycle. In this case, the carried balance should be higher than $10. The carried balance fee can be between $5- $350.

If a borrower pays the balance bi-weekly or semi-monthly, the carried balance fee will be from $5 up to $175. For monthly payments, the fee can be between $10-$350. Below, you can see Elastic’s fee table.

Let’s look at an example to better understand Elastic student loans’ cost. If you have a $500 carried balance, you will pay $15 under the bi-weekly or semi-monthly plans. However, under monthly payments, you will be required to pay $30. Again, keep in mind that the carried balance fee is for each billing cycle, while the cash advance fee is a one-time payment when the borrower requests the money.

It might seem complicated, but once you get familiar with the costing, you will be an expert in calculating how much you need to pay for Elastic funds. Besides, Elastic’s transparency in costing is another sign of its reliability. Additionally, borrowers can use the payment calculator on the Elastic website.

Some Points to Remember

Elastic provides quick cash. If you need money immediately, the application will take a few minutes. It is possible to apply for funds online or by using a mobile application. Besides, the individual can receive the money within one business day.

As attractive as Elastic student loans seem, you should not forget that it is a debt and comes with costs. Having easy access to funds does not mean that you need to request cash every time you feel a need for money or cryptocurrency. Only request cash advances when the expenses are urgent and essential. Moreover, do not request more than what you need.

Eligibility Requirements

Easy money is not accessible to everyone. There exist many requirements that borrowers must satisfy to get cash from Elastic.

First, the borrower has to meet the age of majority requirement. In most states, the age of majority is 18, but there can be exceptions. For example, in Alabama and Nebraska, you need to be at least 19. Besides, you need to live in a state where Elastic operates.

The borrowers who utilized the Military Lending Act cannot apply to Elastic student loans.

The lender checks the reliability of the borrowers. Therefore, the customer needs to prove that he/she will be able to repay the student debt. One of the related conditions is having a stable income source. The borrower can be required to provide supporting documents to verify identity. Having a checking account and agreeing to terms and conditions are also necessary. Lastly, the lender will check the borrower’s credit performance by getting data from third-party vendors.

Application Process

If you want to get the benefits that the Elastic offer, you need to apply online through the official website. Unfortunately, application through the phone is not possible because such methods can expose personal information to third parties. The application process takes a few minutes. The applicants fill in the information regarding their residence, income, and checking account. They should also provide a valid email address and consent for electronic disclosures.

Benefits of Elastic

Before you decide to apply, there are some points to evaluate. Like many student loan alternatives, Elastic also has advantages and drawbacks.

- No interest- one of the benefits of Elastic student loans is that it does not have an interest. When people miss payments in other loans, the banks or federal government charges interest, and they accumulate. Luckily, with Elastic, there is no interest or late payment fee.

- Transparency- Another advantage of Elastic is its transparency. It is possible to view all details of cost on their official platform. There is a table of costs, together with detailed explanations, to inform the potential borrowers and create realistic expectations.

- Multiple Billing Cycles- the lender gives flexibility to borrowers to customize their repayment frequency. As mentioned, borrowers can repay the debt weekly, bi-weekly, semi-monthly, etc.

- Easy/Fast Application- It would be a mistake not to mention the easy and fast application process Elastic provides. It takes a few minutes to complete the application. Besides, the borrowers will get a quick response- approval or rejection- to their application.

The Drawbacks

Unfortunately, there exist some drawbacks to Elastic student loans.

- Expensive- Elastic funds can be a little expensive. If you are going to make a bi-weekly or semi-monthly payment, the minimum payment can be as high as $50. If the principal is less than $50, the entire balance should be paid. The rates can be even higher for monthly payments.

- Not available in all states- The borrowers in need can still be unable to utilize Elastic funds if they live in a state where Elastic does not operate. Currently, Elastic is operating in around 39 states. Besides, it does not have a physical location, which can be important for some borrowers.

Should You Get Elastic Funds?

The bottom line of all the details mentioned above is that if your need is not urgent and important, try to avoid getting quick cash advances. There usually exists no excellent alternative for short-term credit. It will be expensive no matter which company provides it. You need to consider the cost for your immediate cash access.

In case you have more time to apply and receive cash, it is advisable to consider other student loan alternatives. In the following sections, we will discuss these options. If you want to get more information, you can check our blogs or contact Student Loans Resolved experts.

1. Private Loans

It is possible to apply for private student loans instead of cash advances to finance education. There exist many different lenders for student loans. Before choosing one, you need to assess their offers and select the most affordable one.

For example, one of the best student loan providers is Earnest. Its interest rates start from 1.05% and 3.49% for variable and fixed APR, respectively.

However, keep in mind that private loans will require a stable income source and excellent credit performance. Usually, a credit score higher than 600 is desirable. Besides, some lenders can require a cosigner. A cosigner is a third-party individual who can take responsibility if you fail to make payments.

Compared to federal loans, neither private loans, not Elastic student loans are better alternatives. Private loans are usually more expensive for borrowers, and they do not provide debt elimination opportunities like forgiveness programs. Hence, it can be a better idea to check your eligibility for federal loans before even considering other options.

2. Federal Loans

The U.S Education Department provides multiple student loan programs to allow more people to get an education. Hence, the Education Department itself becomes a lender. Currently, there exist four types of federal loans.

Direct subsidized loans are available for undergraduate students. The loan is distributed based on the financial needs. If you are a graduate or professional student, you can apply for unsubsidized loans. This category involves such students, in addition to undergraduate ones. However, unsubsidized loans are not distributed based on financial need.

Another category of federal loans is Direct PLUS. It is available both to graduate or professional students and parents of undergraduate students. Different from other classes, this loan type will require a credit performance analysis of the borrower. Lastly, consolidation loans let borrowers combine multiple federal loans into one direct loan.

Benefits

The maximum amount a borrower can take through federal loans depends on the education level. For example, undergraduate students can get between $5,500-$12,500 through subsidized or unsubsidized loans.

This amount is up to $20,500 for graduate or professional students. Lastly, parents can borrow depending on the educational costs required for the dependent child.

Why Federal Loans are Preferable

There are many elements that make federal loans preferable to Elastic student loans or private loans. First, the interest that federal loans require is usually low and fixed. Therefore, such financing strategies are more affordable. Also, federal loans do not require a credit check. Many people with bad credit performance or no history of credit can qualify for federal debt. Besides, the federal government provides student loans without cosigners.

When it comes to repayment, these loans do not require any payment while a borrower still studies or six months after graduation. The government provides multiple repayment options that allow borrowers to choose the one that suits their finances the best. Especially if you select income-based repayment plans, your monthly payments can even be $0 during financial difficulties.

Additionally, federal debt is subject to many debt eliminations or reduction programs, such as forgiveness opportunities. For example, if you work in the public sector, you might qualify for Public Service Loan Forgiveness. This program will eliminate the rest of the debt once the borrower makes 120 qualifying payments.

What You Should Consider Before Getting Loans

Before you undertake debt obligations, it is necessary to understand that student loans are a legal responsibility that should be repaid with additional interest. Hence, you need to be a responsible borrower and keep track of your loans.

Before getting money, think about how the repayment process will affect your finances and how much you can afford. Your loans should not exceed a small portion of your salary. Otherwise, you would be required to cut other expenses or find additional income sources.

Additionally, before accepting a loan, read the terms carefully and keep all related documents. Whenever you make a payment, save the bills and other papers. In this way, you can prove the payments if any technical issues happen in the future.

Lastly, if you face any financial difficulty, you need to immediately contact the loan servicer or private lender. These parties can help you by providing loan forbearance or deferment options. Otherwise, the interest will accrue, and debt will be more challenging to repay.

Get an Expert Help

If you feel lost among all the options, you can contact third-party debt experts, as Student Loans Resolved. Our experts can analyze your finances and find the best source for elastic student loans.